Thursday, May 5, 2011

U.S. Corn Outlook

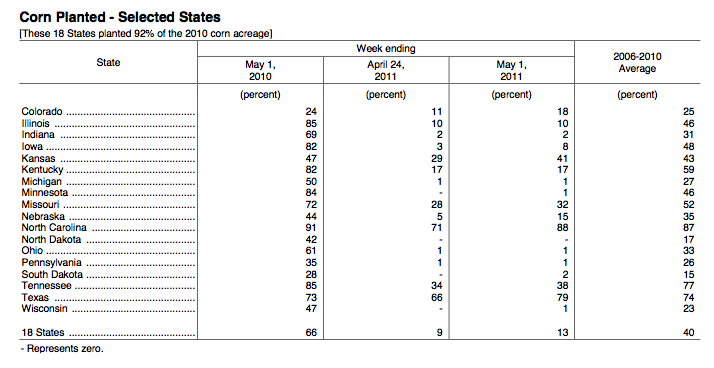

Earlier in the week, we noted that the US corn planting conditions have been suboptimal, with planting pace significantly behind both last year and the five year average for this date. Cold wet weather has slowed field activities, particularly in the northern and central growing regions. The USDA Crop Progress report for the week ending May 1st underdscores this point (see table below). For the primary growing states, 13% of the intended acres were in the ground vs. 66% in 2010. For potential yield modelers, we recommend using a 'late-plant' scenario for 2011. This does not mean that the US cannot make a decent crop this year, but it will highlihght the need for better post-germination weather. We are looking at the cooler weather to give way to a milder and drier pattern over the next few days into next week, so we are expecting some of this gap to be closed over the next two weeks.

(Click charts to expand)

While the broader ags and softs complex has softened recently, there may be a reversal around the corner, particularly for corn. To support this assumption, readers should view the Food and Agriculture Organization (FAO) supply & demand brief which was released today. In the brief, the FAO confirms that the 2010/11 estimated S-D balance has gotten worse approaching the end of the marketing year (see first chart below). In the summary, it states that global cereal production is projected to decrease -1.2% for 2010/11 and this may add some upside risk to prices in the short term.

In addition, the second chart below highlights the difference in cereal prices vs. where they were one year ago as represented in the food commodity price index. The overall price index averaged 232 points in April 2011 (+35% year/year) and the cereal price index averaged 265 points which is an increase of 71% over April 2010.

In light of the tight global S-D situation, even though the USD is showing signs of strength this morning, the broader downward trend that the dollar has displayed emphasizes the upside risk to grain/oilseed prices going forward. Further, the notion of the necessity for 'perfect US weather' that many analysts have been calling for is already being tested, adding to the upside risk. Even with the expectations for larger crops across many of the world's primary origins, demand has not eased and the projection for shrinking grain inventories amid low stock to use ratios should limit downside activity concerning corn prices for July/Sep contracts.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

(Source: http://seekingalpha.com/article/268012-u-s-corn-outlook)

This post was written by: HaMienHoang (admin)

Click on PayPal buttons below to donate money to HaMienHoang:

Follow HaMienHoang on Twitter

0 Responses to “U.S. Corn Outlook”

Post a Comment